AUTHOR

Arcadis made a probing contribution to the global discussion on the pathway to net-zero carbon emissions last week.

Supercharging Net Zero is an economic modelling study that sets out in detail the steps that 10 different countries – Australia as well as the United States, China, UK, the Netherlands, France, Germany, Belgium, India and Brazil - would need to take to transition to net zero by 2050, in time to limit global warming to 1.5.

The Arcadis study comes close on the heels of the IPCC’s report released in August that signalled a Code Red for humanity, arguing that warming of 1.5°C was inevitable.

Sadly, Supercharging Net Zero seems to confirm that the transition pathways to net zero for the major economies surveyed are indeed impossibly steep.

Assuming all 10 countries surveyed were aligned on the need to cut emissions (not yet the case) and used all the levers at their disposal to do so, the study suggests they would need to have halved carbon emissions by 2029 to have a hope of reaching net zero by 2050. Australia would need to halve emissions within two years, and most countries within four.

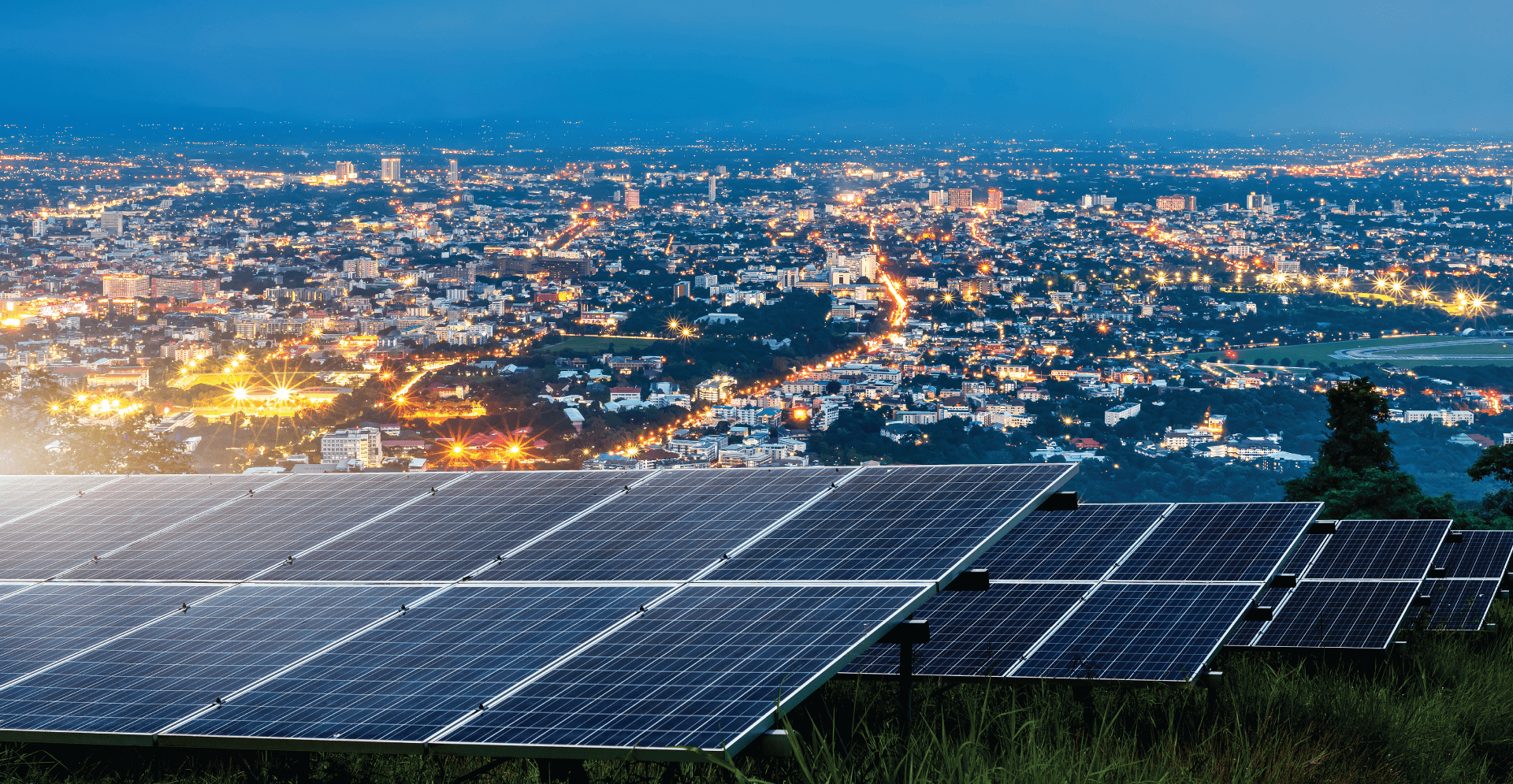

Arcadis’ modelling also showed that the 10 countries surveyed would need to invest a combined $9.9 trillion in renewable energy capacity within the next decade to accommodate growth in energy demand while making the necessary emissions reductions. Australia alone would need to invest $165 billion in renewables, development of workable carbon capture and storage, and upgrades to the power grid in the same period.

While that’s an astounding investment opportunity, it’s unfortunately in the context of a transition pathway that looks ominously unrealistic.

Should we despair? Not yet. I prefer to see Supercharging Net Zero as a reality check highlighting (a) the urgency of stepping up efforts to reduce emissions and (b) the need to start planning for the reality of climate impacts. In other words, a warning that we need to be able to walk and chew gum at the same.

Getting policy consensus on the way forward in our response to climate change has proved diabolically difficult in Australia over the past decade or more. But we are fast running out of options and right now, a few things seem unavoidable if we are to meet the challenge of climate change.

The first is pricing carbon. A low-emissions economy needs price signals and the most important is a price on the externality of carbon. And it is It is increasingly clear that if we don’t do it ourselves it will be done to us.

Carbon tariffs are a reality and Australia is deeply enmeshed in the global economy and trade system. Australia’s own contribution to global warming may be relatively small but that’s not so for much of our resource and energy exports (counted as Scope 3 emissions). Our major resource companies know it and are working hard at neutralising not only Scope 1 and 2 emissions but also Scope 3, pricing in the carbon impact at every step in the downstream supply chain.

Australia’s trade-exposed industries are already building in carbon pricing as other countries accelerate their own transitions to net zero. Surely it would be simpler to apply a carbon price consistently across the economy.

Secondly, policy alignment and co-ordination across all levels of Government is critical to providing a framework for the wider economy to reduce emissions. Polls show the public wants action. In the absence of a national framework, corporates, industries, capital markets, states, territories and local governments are having to forge their own path. The result is a patchwork of regulation and incentives that do not always mesh well; look no further than divergent state Government policies on electric vehicles and renewable energy targets.

Thirdly, as the IPCC’s analysis shows and Arcadis’ study would seem to confirm, we appear destined for a world that is on average at least 1.5°C warmer. We need to start planning accordingly. What does this mean for sea levels and inundation in our coastal areas? What will longer, more frequent droughts mean for agribusiness, one of our key industries? What will more extreme weather events – floods, cyclones, fires - mean for the built environment and insurers?

Arcadis is already working with clients on building resilience into the planning of critical infrastructure and supply chains, as a key strategy for mitigating climate risk. Think of it as an insurance policy against the more severe impacts of climate change.

If we needed it, Supercharging Net Zero is another sobering reminder of the challenges we face in transitioning the global economy to carbon neutrality. It is a steep mountain to climb but we cannot afford to lose sight of the peak.

AUTHOR